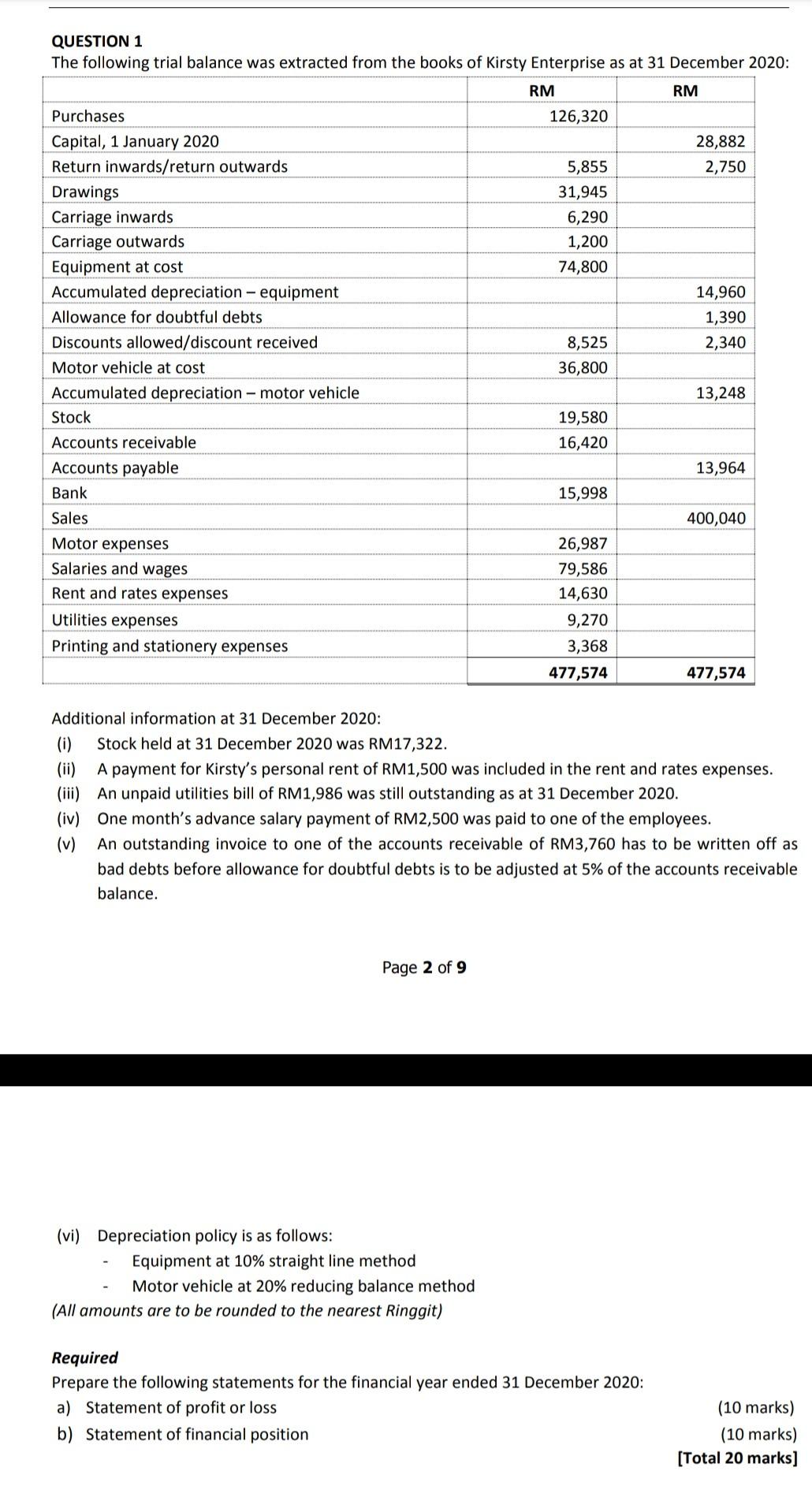

My partner and i keeps on the 40K within the personal credit card debt, and additionally a mortgage fee and figuratively speaking. Our company is working hard to pay off it personal debt and you will have been moving in just the right direction. We got recognized for a 30K unsecured loan in the a lower life expectancy interest (8%) than just our playing cards. I’m questioning if there’s any worthwhile reasoning to not do this.

- I plan on having fun with 100% of your financing to repay higher-attention playing cards

- We have budgeted to spend more than minimal monthly

- The reduced rate of interest is actually closed in, bringing do not skip a couple of straight money (our company is diligent into the using costs and never too worried about this)

- We both features stable a position, assuming anything wade better i anticipate a boost in income (though needless to say perhaps not counting on which)

- I’ve little or no disaster offers

- We have some relatives safety nets from inside the a worst-instance scenario

- Our credit is quite a great

- I no more fool around with one credit cards except one to shop cards that’s paid-in full each month. I have repaired our purchasing patterns and you may all of our obligations try moving in the correct guidance.

11 Responses eleven

You happen to be lost how come you happen to be $40K during the CC obligations. We were $30K when you look at the CC personal debt as we didn’t payday loans online Carbon Hill see where all of our currency ran.

Comprehending that — and you may strictly staying with a resources when you are strong in debt — is actually the answer to all of us escaping. Everything else is kicking brand new can also be down the road.

is that you are capable security a lot more minimal payments on your own cards/loans: you are whittling out on overall debt, however it is a reduced procedure. Pulled along with: